The Global Agenda 2025: Memos to Policymakers

Service Sector Growth is Essential to Escaping the Middle-Income Trap

The modern Chinese miracle and its state-led growth has centered on the party-state system forcing provincial government officials into a GDP tournament, where success is measured in increasing growth and rewards are handed out in the form of promotions. Short term limits for officials have encouraged massive investment into physical capital to stimulate immediate growth. While this is great for growth in manufacturing, it is not sufficient for building an advanced, educated economy based on human capital, high-tech science, and a robust service sector. We can already see the consequences of the myopia of the tournament model, where officials invest mainly in the quick returns of physical capital, piling too much money into real estate and infrastructure.

As Chinese growth slows, the state’s strategy of directing capital towards physical investment has reached a stage of greatly diminishing marginal returns. The kind of performance necessary for fostering economic growth in the next phase of development cannot be incentivized with the relatively unsophisticated GDP tournament. China must develop a service sector-first strategy to get out of the middle-income trap.

Consider the case of German economic growth in the late 19th and early 20th century. Like China, Germany was a rapidly growing continental power with a state-led industrial policy competing with a liberal hegemon. Germany had already achieved industrial productivity parity (or even superiority) with Britain by 1871 despite having only 75 percent of the GDP per capita. The main thing that held Germany back was the service sector. It was only by steady improvements in service-sector productivity over the next 60 years was Germany able to surpass Britain. History tells us that for scientifically sophisticated and politically competent countries like Germany or China, manufacturing is the easy part. If China wants to achieve parity with the Western world, where services make up around 70% of GDP, they will have to increase their service output, which remains at around 50%.

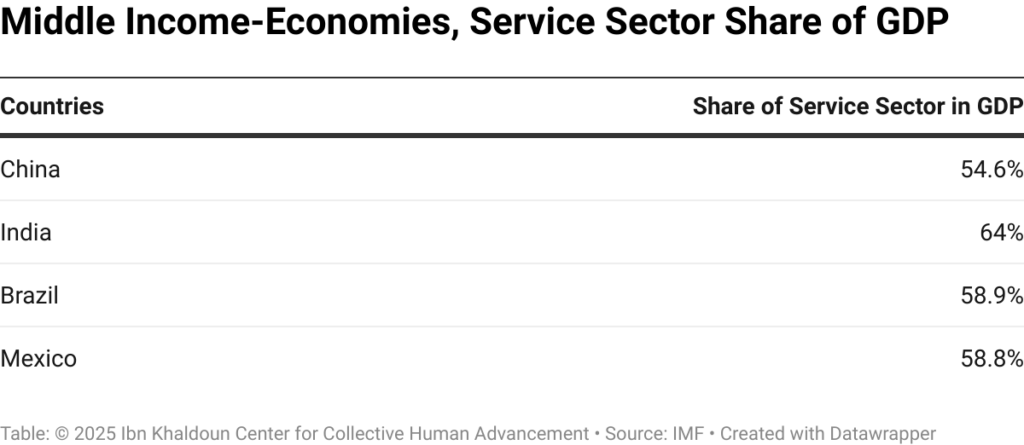

China not only lags high-income economies but also developing economies when it comes to service sector share of the GDP.

The service sector can’t be developed quickly by short-term economic planners. It must be fostered over the long run by private actors who meet actual demands through a better developed and dynamic finance sector, decreased reliance on agriculture to free up excess labor, and more human capital.

Finance needs to flow into socially productive services unimpeded. Access money, as Ang argues in “China’s Gilded Age” (2020) may allow corruption to work in service of manufacturing growth, but a service sector run on access money will not select profitable or productive services as efficiently as the market. Inefficient agricultural labor, locked in place by underinvestment in rural China and arbitrary labor mobility restraints like the Hukou system, needs to be phased out. That labor is better used in cities, staffing the services that grow GDP, and can generate demand for even further service sector growth. Moreover, the typical formula of using a state-led financial system to select profitable ventures needs to be replaced with an independent finance system that funds profitable firms. Finally, an educated workforce with relevant skills has to be fostered, which, given the model in Galiani et. al’s 2008 paper, can be done before developing a vast service sector. This is the front on which China is doing the best, and it appears that China’s middle class has enough wealth to demand the services and the education to staff a service sector.

Many developing countries like Indonesia, Brazil, India, and even Mexico lag the advanced economies in service sector growth. Middle-income emerging economies cannot become high-income developed economies without productivity growth in the service sector. Productivity in manufacturing is the first step, but if they cannot channel the returns from manufacturing into the institutions, education, and policy making needed to nurture the service sector, they will fail to escape the middle-income trap.

Local investors sit in front of the electronic board showing shares index at a securities company in Chengdu, in China’s southwestern province of Sichuan, on March 25, 2008. (LIU JIN/AFP via Getty Images)